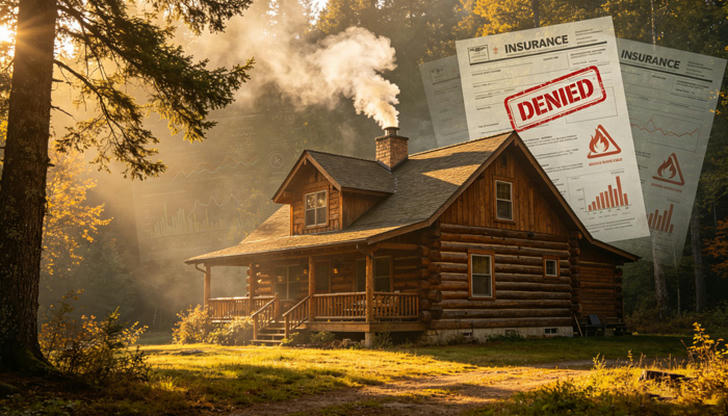

Your Log Cabin May Not Be Insurable-Here's Why

For many buyers, a log cabin is the perfect escape---quiet forests, simple living, and a home that feels far from modern stress. But after the excitement of buying or building one, a surprising problem can appear: insurance.

In some cases, homeowners discover their cabin is expensive to insure. In more extreme situations, it may be difficult---or even impossible---to get standard coverage. The issue is not the cabin's charm or quality. It's how insurers are redefining risk.

The Silent Shift in Home Insurance

Home insurance used to be relatively predictable. If a house was built to code and located in a reasonable area, coverage was usually available. But over the past few years, insurers have been quietly rewriting their risk models.

Instead of focusing only on construction quality, companies are now heavily weighting environmental exposure, disaster probability, and long-term climate data. That shift has hit rural and forested properties especially hard.

Log cabins---often located in scenic, wooded, or remote areas---now frequently fall into higher-risk categories, regardless of how well they are built.

Wildfire Risk Has Changed the Rules

One of the biggest drivers behind this shift is wildfire risk.

In many Western states, wildfire seasons are longer, hotter, and more unpredictable than they were a decade ago. Entire communities have experienced rapid evacuation events and large-scale property loss.

Because log cabins are typically constructed with a high percentage of wood, insurers view them as more vulnerable in fire-prone regions. Even when owners take precautions, the surrounding environment often determines the insurance outcome more than the structure itself.

In some wildfire-prone zones, insurers have reduced coverage options, raised premiums dramatically, or exited the market entirely.

Location Now Matters More Than the Cabin Itself

A surprising reality for many buyers is that two identical log cabins can receive completely different insurance decisions based solely on location.

Insurance companies now analyze ZIP codes, wildfire maps, terrain elevation, vegetation density, and historical disaster data. A cabin in one forested valley may be fully insurable, while another just a short distance away is considered too risky.

This creates a new kind of paradox: the more beautiful and remote the setting, the harder it may be to insure.

What used to be a selling point---seclusion, forest access, mountain views---is now a potential liability in underwriting models.

Emergency Access and Infrastructure Are Critical Factors

Beyond wildfire risk, insurers also evaluate how easily emergency services can reach a property.

Key considerations include:

- Distance from the nearest fire station

- Road conditions (paved vs. gravel or seasonal access roads)

- Water availability, such as hydrants or reliable water storage

- Response time estimates for emergency crews

A log cabin that looks ideal for off-grid living may be viewed as high risk if firefighters cannot easily reach it during an emergency.

In other words, insurance companies are not just assessing the building---they are assessing whether the location can realistically be saved in a crisis.

Rising Reconstruction Costs Are Driving Up Risk

Another factor shaping insurance decisions is the cost of rebuilding.

Log cabins are not always "cheap rustic homes" anymore. Depending on design and materials, they can be expensive to reconstruct, especially with today's lumber prices, labor shortages, and stricter building standards.

From an insurer's perspective, this creates a double risk:

- Higher likelihood of environmental damage in certain regions

- Higher payout cost if the property is destroyed

As a result, premiums rise, deductibles increase, or coverage is restricted altogether.

Climate Volatility Is Reshaping the Entire Market

Wildfires are only part of a larger trend. Floods, hurricanes, and extreme weather events are also increasing in frequency and severity across the country.

In some states, insurance companies have already reduced coverage availability or limited policies in high-risk zones. This has created uncertainty for rural homeowners, especially those in scenic but environmentally exposed areas.

For log cabin owners, this means insurance is no longer just a formality---it is part of the long-term feasibility of owning the property.

Some Homeowners Are Adapting to Stay Insurable

Despite these challenges, many cabin owners are adjusting their properties to meet modern insurance expectations.

Common strategies include:

- Creating defensible space by clearing vegetation around the cabin

- Installing fire-resistant roofing and treated wood materials

- Adding monitored fire detection systems or sprinkler systems

- Improving road access for emergency vehicles

- Documenting maintenance and safety upgrades for insurers

In some cases, these improvements can make the difference between approval and rejection.

Location selection is also becoming more strategic. Buyers are increasingly prioritizing insurance-friendly regions rather than purely scenic ones.

The Hidden Cost of the Modern Cabin Dream

What surprises many first-time buyers is that insurance is no longer a one-time checkbox---it's an ongoing cost that can significantly affect affordability.

Even when coverage is available, premiums in higher-risk areas can add thousands of dollars per year. Over time, this changes the economics of owning a remote cabin.

Some homeowners also find themselves pushed toward specialty or surplus-line insurers, which can offer coverage but often at higher prices and with more restrictions.

The "cheap escape home" narrative doesn't always match today's reality.

The Cabin Dream Isn't Gone---But It Has Evolved

Despite all these challenges, log cabins are not disappearing. If anything, demand remains strong. People still want quiet spaces, natural surroundings, and a break from urban density.

What is changing is the definition of a "safe" cabin investment.

Today, owning a log cabin is no longer just about design or lifestyle. It's about understanding environmental risk, insurance availability, and long-term sustainability.

The modern cabin dream still exists---but it now comes with a new requirement: planning not just for where you want to live, but for whether the system will allow you to stay protected there. .md